The economic ups and downs of 2022 continued through spring 2023. Inflation remains relatively high, but decreasing, interest rates continue to climb, the labor market remains strong, and slowing economic growth fostered uncertainty regarding future growth. In addition, spring 2023 witnessed a major bank failure and continues to endure the unresolved debt ceiling saga. This report will provide a brief look into the performance of the major economic benchmarks and issues that occurred in spring 2023.

Economic Growth in Historical Perspective

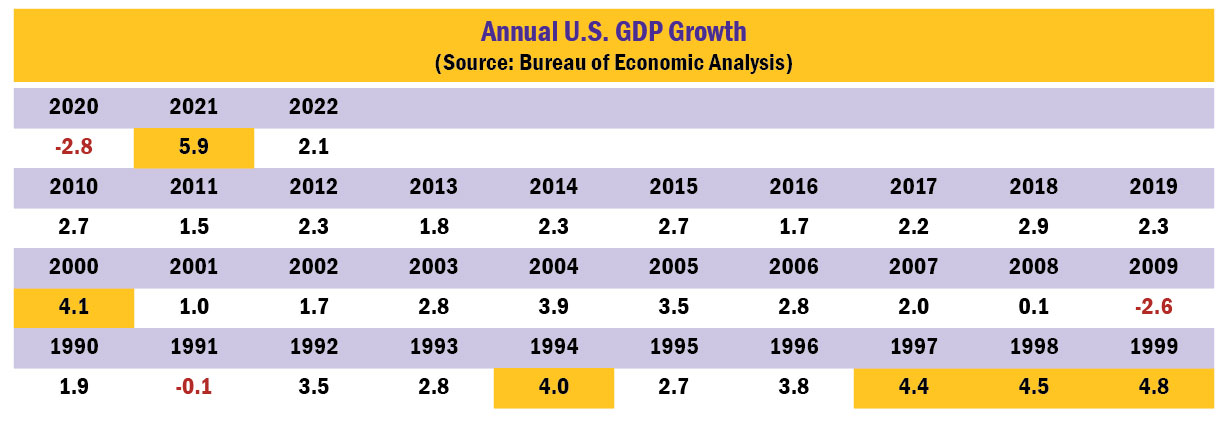

The table below provides U.S. economic growth since 1990. Economic growth is measured by changes in the Gross Domestic Product (GDP), which is the value of goods and services produced in the U.S. over a stated time period. The best years for economic growth, when growth was 4.0% or greater, are highlighted in yellow. Negative growth years are indicated in red.

Summarizing economic growth since 1990:

1990s – after a slow start, the internet and technological innovation fueled the strongest decade for economic growth with four years exceeding 4%.

2000s – after strong growth to start the century, the economy slowed significantly due to downturns in manufacturing and technology combined with Sept. 11. Economic growth recovered but was short lived as the financial crisis took hold in late 2007.

2010s – the longest period of economic growth in U.S. history, but it was a long period of generally low economic growth. Economic growth never exceeded 3%. A temporary boost in 2018 due to tax cuts but economic growth slowed in 2019.

2020s – 2020 worst year for economic growth since the post-World War II economic contraction in 1946; 2021 was the best year for economic growth since 1984. The 2020 economic decline was staggering relative to the financial crisis. During the financial crisis, approximately 8.7 million jobs were lost over two years. During the COVID crisis in 2020, 22.3 million jobs were lost over two months. Economic growth was mixed in 2022, with quarterly growth and declines.

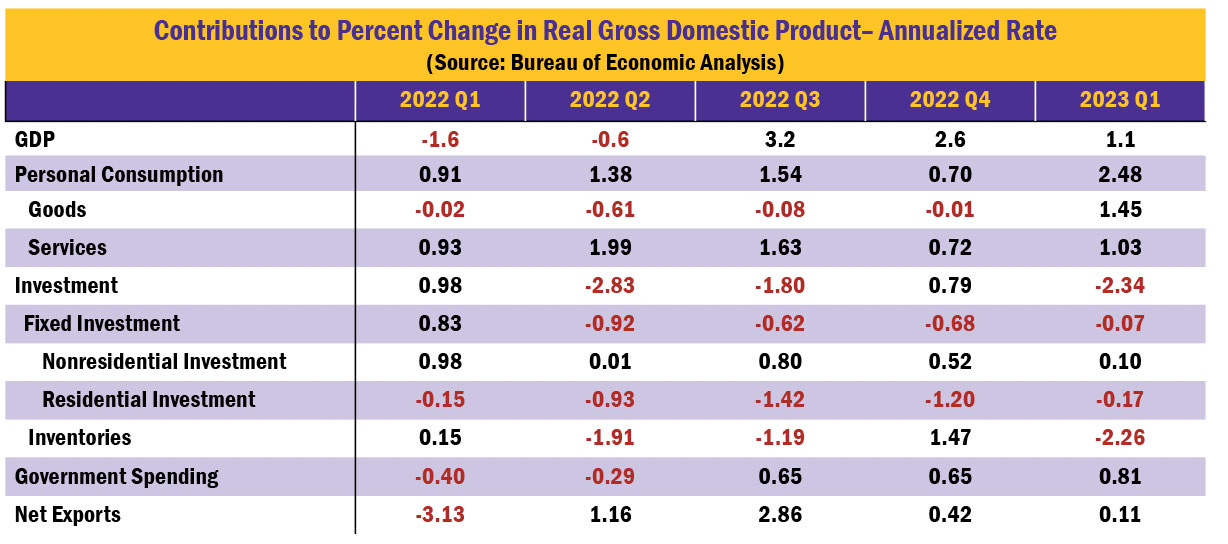

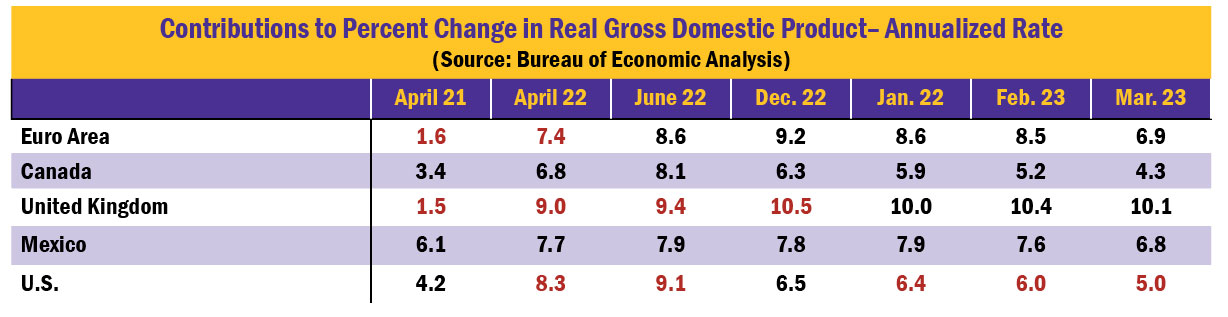

The table below shows how changes in the four components of GDP (personal consumption, investment, government spending and net exports) contributed to the change in quarterly U.S. economic growth since 2022. Personal consumption is split between consumption of goods and consumption of services. Investment is split between fixed investment (residential and nonresidential) and inventories.

2022 was a mixed year for U.S. economic growth, with negative growth in the first two quarters of the year and positive growth in the last two quarters. The first quarter negative growth was unusual, as both personal consumption and investment increased but an abnormal surge in imports drove the economic decline. The surge in imports was due to multiple factors, including a U.S. economy that recovered more robustly than foreign economies, and scaling up of imported goods by business to avoid supply uncertainties created by the Russian invasion of Ukraine and any recurring COVID shutdown by China. A significant drop in investment spending, both residential investment and inventories, was the primary factor causing the drop in second quarter growth. The abnormal first quarter surge of imports was reversed in the third quarter, which combined with increased personal consumption to return positive economic growth. Economic growth continued but slowed in the fourth quarter, led by increases in both personal consumption and investment spending. Economic growth slowed further in the first quarter of 2023, to only 1.1%. Consumer spending once again was the primary driver of the increase, but investment spending declined sharply led by a significant drop in inventories.

Despite rising interest rates in 2022 and 2023, personal consumption remained strong, positively contributing to GDP growth in every quarter. In 2022, personal consumption generally shifted toward services rather than goods, as consumption of goods declined in every quarter while consumption of services increased. That changed in the first quarter of 2023, which saw increases in both the consumption of goods (led by motor vehicles and parts) and services. Since the first quarter of 2022, non-residential investment has increased slightly in each quarter, but residential investment declined. Growing economic uncertainty contributed to ups and downs in inventory spending, with the first quarter 2023 decline led by decreases in inventory investment in both wholesale trade and manufacturing.

Financial Markets

What do the financial markets indicate about the possibility of an upcoming recession? The answer is: there might be a recession, but then again there might not be a recession.

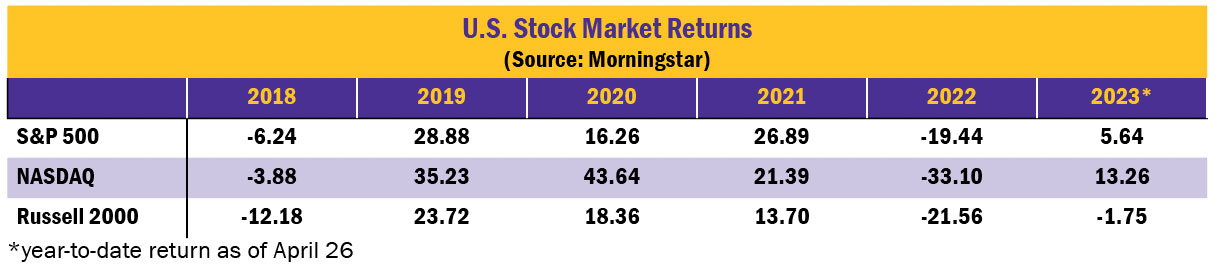

The table below shows the annual returns of three major U.S. stock indexes since 2018: 1) the S&P 500 – a diversified index that measures the stock performance of 500 relatively large companies (it is a “large-cap” index, generally comprised of companies having a total stock value exceeding $10 billion), 2) the NASDAQ – an index comprised of over 3000 companies listed on the NASDAQ stock exchange and heavily weighted toward technology, and 3) the Russell 2000 – a diversified index that measures the stock performance of 2000 relatively small companies (it is a “small-cap” index, generally comprised of companies having a total stock value less than $2 billion). For comparative purposes, the long-run average annual return (since 1926) is approximately 12 percent on large-cap stocks and 16 percent on small-cap stocks.

Stock prices reflect expectations of future profitability. Theoretically, the stock market is a leading economic indicator. After an abysmal 2022 reflecting growing economic uncertainty and rising interest rates, stock market performance, although somewhat mixed, has generally rebounded in 2023 and appears to reflect at least some economic optimism. In particular, the S&P 500 and NASDAQ have posted relatively good year-to-date returns through late April, with the S&P 500 up over 5% and the NASDAQ increasing over 13%. However, the Russell 2000 was slightly down, and a decline of 1% in March retail sales reflected a slowing economy and contributed to economic uncertainty.

Contrary to the somewhat mixed signals of the stock market, the bond market tells a different tale regarding economic expectations. Historically, the yield curve has been a pretty good indicator of pending recessions. The yield curve is a graphical representation of the term structure of interest rates. In other words, the yield curve shows the relationship between short-term and long-term interest rates for securities with equal default risk, but different maturities. The yield curve is “inverted” when short-term rates are greater than long-term rates. Specifically, the spread (difference) between the yield on long-term (ten-year) U.S. Treasury securities and the yield on short-term (either 2-year or 3-month) U.S. Treasury securities has been used as a predictor of recessions, with an inverted yield curve generally signaling a pending recession. Both measures have been referenced in the financial and business media as predictors of recessions. Both measures have been excellent predictors of recessions, but not perfect.

The chart below shows the Treasury yield curve on April 26, 2023. Both the 2-year and 3-month yields have recently been greater than the 10-year yield; each comparison would predict an upcoming recession. The yield curve was slightly inverted when the 10-year yield (3.43%) is compared to the 2-year yield (3.90%), and when the 10-year yield (3.43%) is compared to the 3-month yield (5.16%).

A significant reason an inverted yield curve can potentially predict a recession is why an inverted yield curve occurs. Generally, the yield curve slopes up (long-term interest rates are generally higher than short-term interest rates). There tends to be more inflation in the long-term, and investors and lenders need to be compensated for the higher inflation. In addition, there is generally greater economic risk that attaches to the long-term. As a result, in the U.S., long-term interest rates are usually higher than short-term interest rates.

An inverted yield curve, when short-term interest rates are higher than long-term interest rates, reflects increases in short-term interest rates and an expectation that inflation (and interest rates) will decrease in the long-term. The usual cause of increasing short-term interest rates is a change in Federal Reserve policy. The Federal Reserve increases short-term interest rates to bring about an economic slowdown to fight inflation. The Federal Reserve targets the federal funds rate, a very short-term interest rate, which is the overnight borrowing rate between banks. Increasing the federal funds rate can lead to an economic slowdown (and inverted yield curve), but too much of an economic slowdown can precipitate a recession. While an inverted yield curve has historically been a very good indicator of pending recessions, it is not foolproof, and cannot predict the duration and severity of recessions.

Inflation

The table below shows the annualized inflation rate for Europe, Mexico, the United Kingdom, Canada, and the United States for selected months in 2022 and spring 2023 compared to April 2021. Note that the trends in price increases are similar across most countries, with relatively low inflation in April 2021 transitioning to relatively high inflation in 2022. Global factors have impacted global prices, including spikes in oil and wheat prices that resulted from Putin’s invasion of Ukraine, and supply chain issues. Record levels of inflation occurred around the world.

Generally, in 2023, global inflation slightly decreased as supply chain issues faded and energy and food markets stabilized. (The U.K. faces the unique economic challenges that have arisen since Brexit.)

Although inflation remains relatively high in the U.S. compared to historical levels, the 5.0 percent inflation rate for the 12 months ending March 2023 was the smallest 12-month increase since the period ending May 2021. The March 2023 annualized inflation rate reflects increased product input prices, a strong labor market, fluctuating commodity prices, and strong corporate profitability over the previous 12 months.

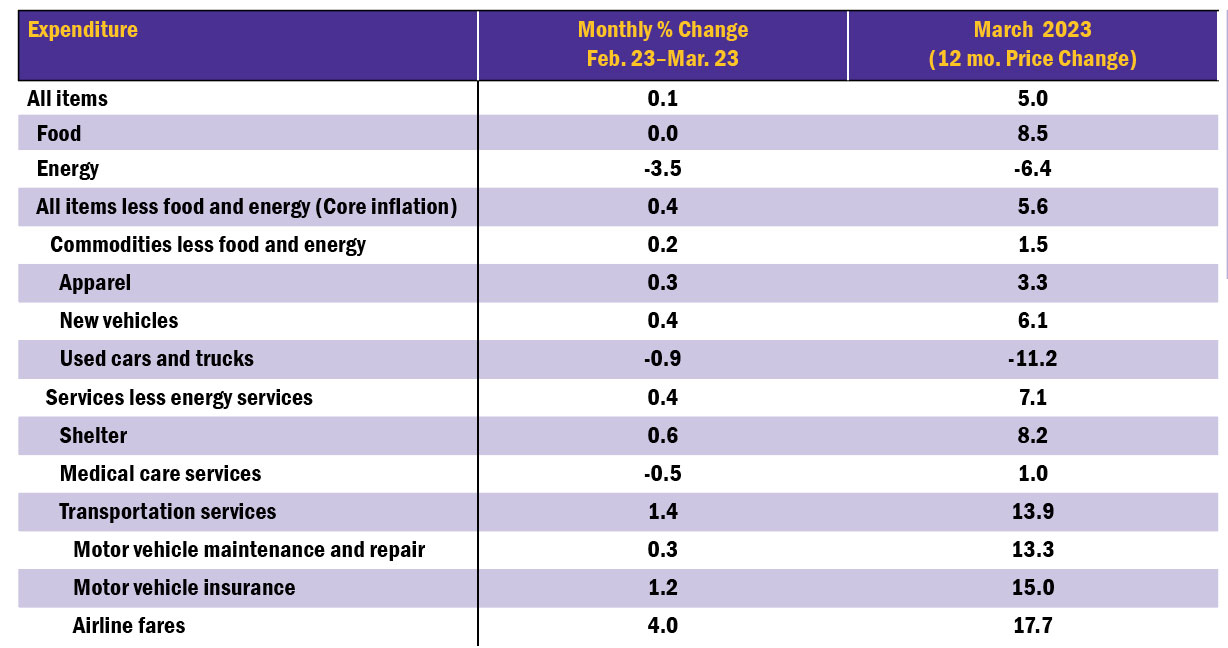

The table below shows price changes for selected products over the 12-month period ending in March 2023 and the seasonally adjusted monthly price change in March compared to February. Major product categories include Food, Energy, and all items less Food and Energy (which is also called “core inflation”). For the 12-months ended March 2023 overall inflation declined to 5.0%, with core inflation (all items less food and energy) at 5.6%.

Food prices increased 8.5% for the 12-month period ended March 2023, though food prices were relatively unchanged in March after increasing 0.5% and 0.4% in January and February, respectively. Energy prices decreased 6.4% over the 12-month period and dropped 3.5% in March, but unexpected announced cuts in oil production by OPEC in early April have caused uncertainty in future energy pricing. New vehicle prices, Shelter, and Transportation Services all had significant increases over the past year at 6.1%, 8.2%, and 13.9%, respectively. New vehicle prices rose 0.4% in March after increasing 0.2% in both January and February. Shelter, which includes housing and rent prices, rose 0.6% in March after increasing 0.7% and 0.8% in January and February, respectively. The index for shelter was by far the largest contributor to the monthly all items price increase. Within Transportation, motor vehicle maintenance and repair, motor vehicle insurance, and airfares all posted double digit price increases over the past 12 months, with airfares posting the highest monthly price increase in March at 4.0%.

Interest Rates

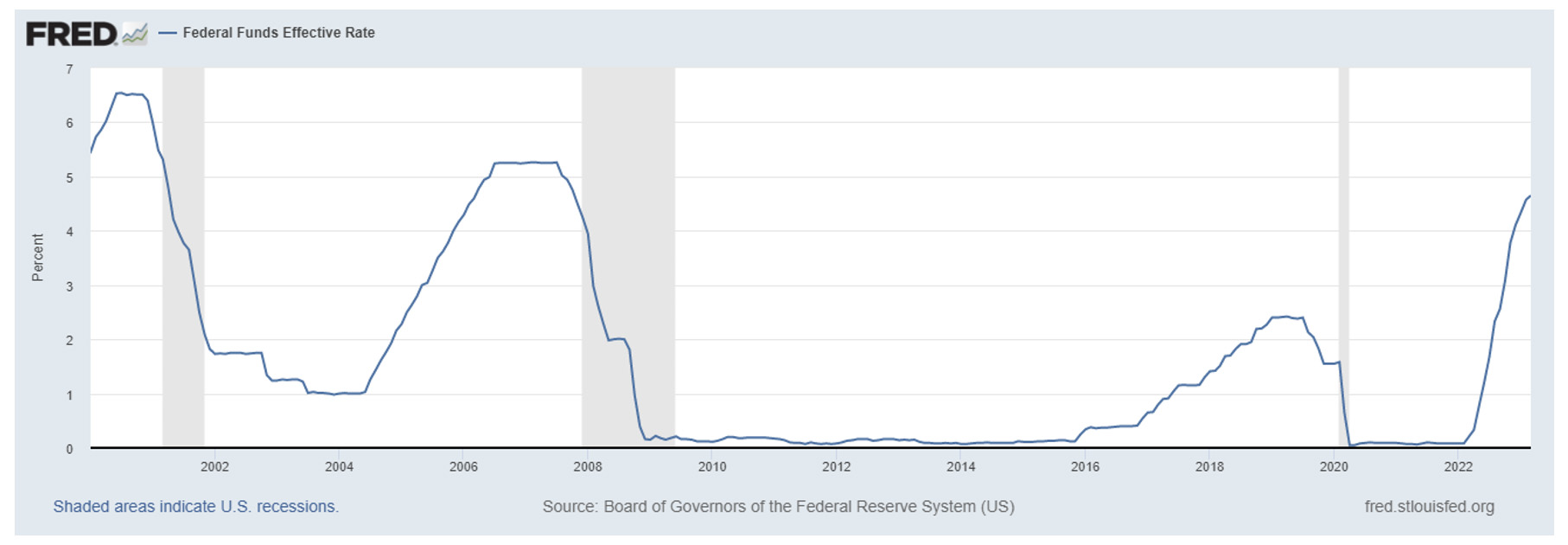

In 2023, the Federal Reserve continued the upward trek for interest rates by increasing the federal funds rate in the first quarter. Theoretically, the Federal Reserve acts in an independent manner to balance economic growth with inflation. The Federal Reserve tries to accomplish this goal through targeting the “fed funds rate” – a very short-term interest rate that when changed, typically has a rippling effect through the financial markets. In early February and again in late March, the Federal Reserve increased the federal funds rate by 25 basis points. That brought the target rate to 4.75 – 5.00%, the highest it has been since 2006. The 2023 rate increases follow seven rate increases in 2022, including a record four times in which the rate was increased by 75 basis points. The federal funds rate has increased significantly since the beginning of 2022, when the rate was at a record low 0.00 – 0.25%. The chart below shows the federal funds effective (market) rate since January 2000.

Federal Funds Effective Rate

It’s all about inflation when it comes to the Federal Reserve increasing interest rates. Certainly since 2020, there are factors that the Federal Reserve cannot control that have played a significant role in contributing to inflation, such as the war in Ukraine, supply chain issues, and avian flu. However, the Federal Reserve can influence the overall level of demand in the economy through strongly influencing interest rates. The primary tool that the Federal Reserve has to combat inflation is through increasing the fed funds rate, which in turn increases borrowing costs and lowers consumer and business demand. Central banks around the world, including the United States, Europe, the United Kingdom, and Canada, have all raised interest rates to combat inflation.

In March, the Federal Reserve projected the fed funds rate to be 5.1% at the end of 2023, signaling that the rate increases of the first quarter were not expected to be the last for the year. The Federal Reserve projected rate decreases in 2024, with the fed funds rate declining to 4.1% by the end of 2024. Of course, the rate projections are subject to changing economic conditions.

Employment and The Job Market

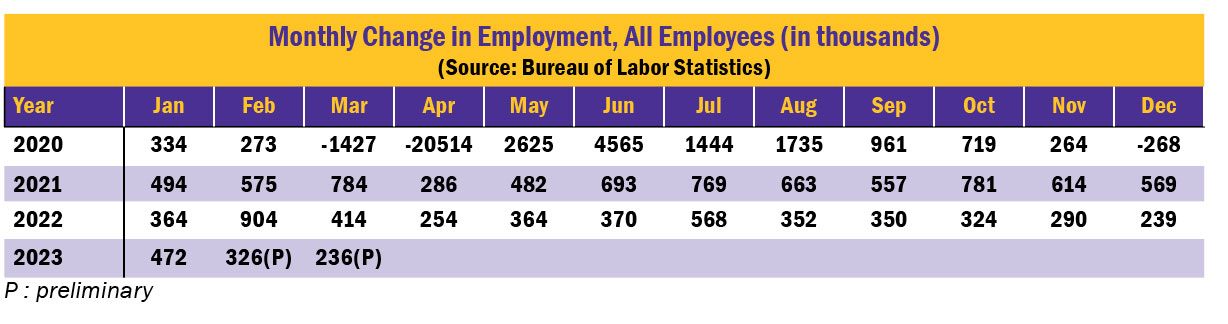

Although interest rates have been rising and uncertainty persists regarding economic growth, the job market has remained strong. The table below shows the monthly change in total nonfarm employment since 2020. In 2020, the onslaught of COVID caused total employment to decrease by over 20 million in April 2020. Employment growth rapidly increased with the economic rebound beginning in May, but by the end of the year the economic rebound had slowed. Job gains were reduced each month beginning in September, with job losses occurring in December. However, job growth returned in January 2021, and employment gains were recorded in every month between January 2021 and March 2023.

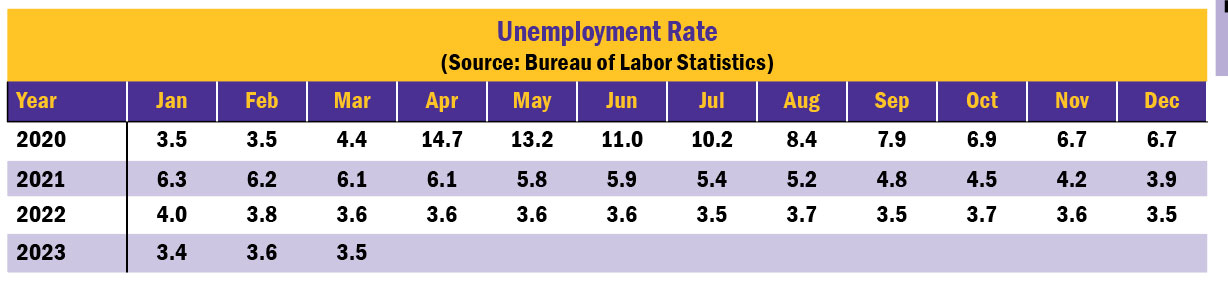

The table below shows the unemployment rate since 2020. Prior to the onset of COVID, the unemployment rate bottomed out at 3.5% in February 2020, the lowest unemployment rate since 1969. After skyrocketing to 14.7% only two months later in April, the unemployment rate began declining in May but was still at 6.7% in December 2020, significantly above the pre-COVID low. In 2021 a gradual decline in the rate continued, and by July 2022 the rate finally returned to its pre-COVID low of 3.5%. In 2023 the rate has remained extremely low, registering 3.4% in January which beat the pre-COVID low. The unemployment rate was still at only 3.5% in March.

The strength of the job market is also indicated through the chart below, which shows the number of unemployed workers per job opening since 2008. The number of unemployed workers to job openings has been less than one since June 2021, lower than at any other time this century. In other words, there were approximately two job openings for every one person unemployed. “Labor shortages” appeared in many industries, leading to a relatively strong increase in wages in both 2021 and 2022. According to the Federal Reserve, in July 2022 the three-month moving average of median wage growth was at its highest level of the century at 6.7%. Although wage growth has decreased slightly from its peak, in 2023 wage growth still exceeded 6% between January and March.

Number of Unemployed Persons per Job Opening

The Housing Market

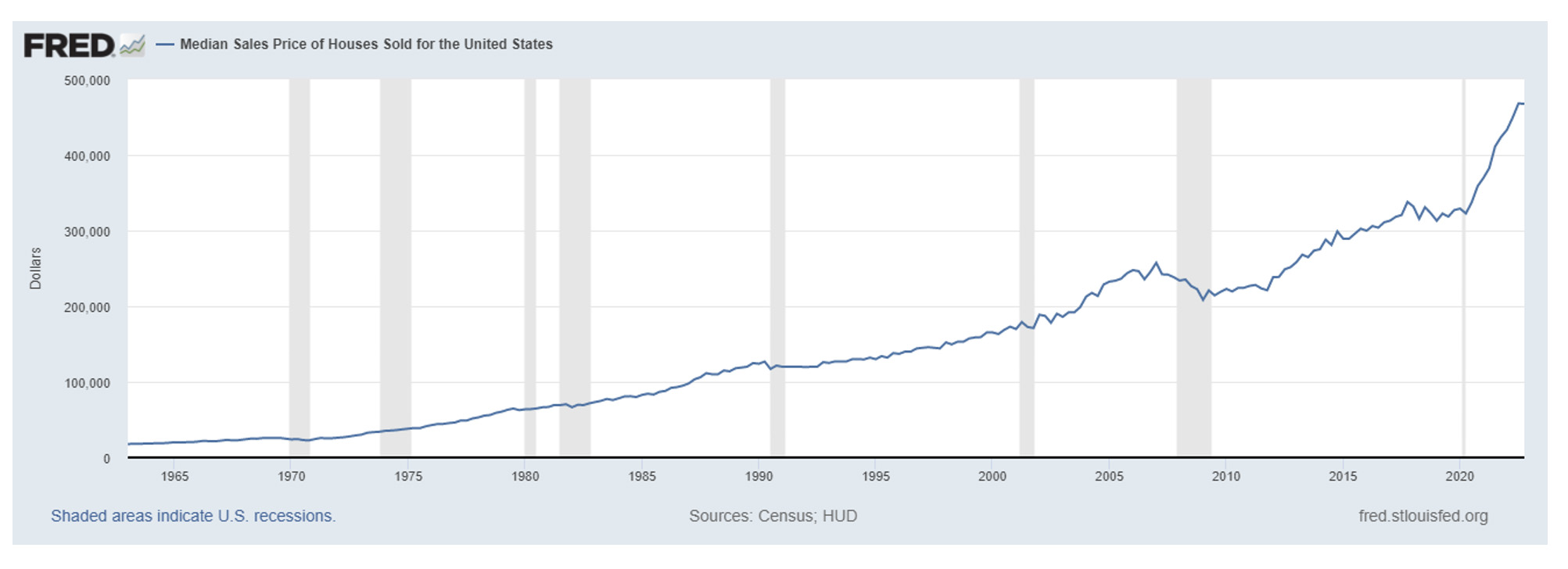

Historically, housing prices have gradually and consistently increased over time. The graph below shows the quarterly median sales price of houses sold in the U.S. from 1963 through 2022. Housing prices generally increase, although exceptions have occurred. A slight dip in prices occurred during the recessions of 1982 and 1991 and the economic slowdown of 2019. Most notably, prices declined significantly during the financial crisis of 2008.

Although housing prices generally increase, beginning in 2020 and continuing through the summer of 2022 the rate of price increases was historically high. Note the steepness of the curve beginning in 2020. Between the first quarter of 2020 through the second quarter of 2022, the quarterly median sales price increased approximately 42%. The percentage increase in prices over those ten quarters nearly matched the percentage increase that occurred over the entire last decade. Between the first quarter of 2010 and the fourth quarter of 2019, the quarterly median sales price increased approximately 47%.

Quarterly Median Sales Price of Houses Sold in the United States, 1963 – 2022

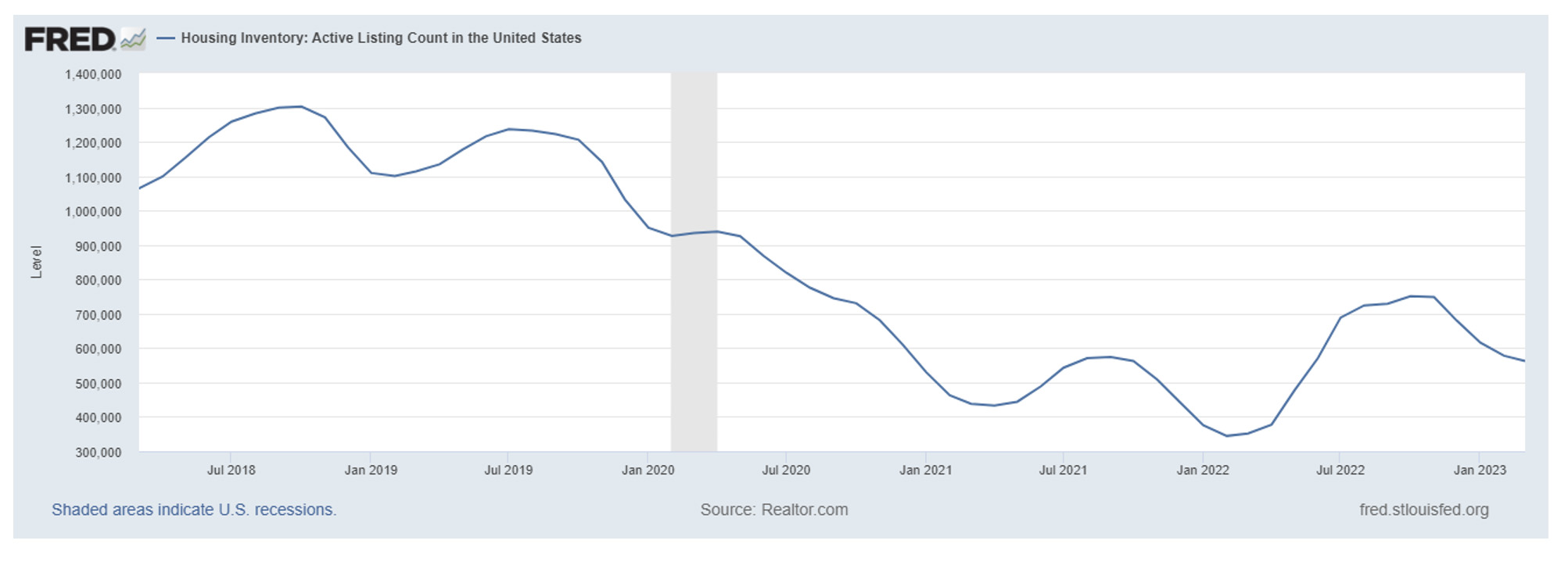

The graph below shows the supply of houses available for sale from March 2018 through March 2023. Generally, the active listings for houses declined significantly beginning in early 2020. Low mortgage rates, combined with relatively low housing inventory, helped fuel the rapid increase in home prices between the first quarter of 2020 and second quarter of 2022.

Housing Supply: Active Listings March 2018 – March 2023

Source: Realtor.com, retrieved from FRED, Federal Reserve Bank of St. Louis

Rising mortgage rates began to impact housing prices and sales in the second half of 2022. According to the National Association of Realtors (NAR), the national median existing-home sales price fell in January 2023 for the seventh straight month to $361,200, a decline of nearly 13% from the June 2022 price peak. However, after declining for 12 straight months, existing-home sales jumped 14.5% in February 2023, which contributed to an increase in the median existing-home sales price to $363,000. The jump was short-lived, with existing home sales declining 2.4% in March, down 22% compared to one year ago. The median existing-home sales price increased slightly in March to $375,700 but was still 0.9% lower compared to March 2022.

Silicon Valley Bank

The financial markets were recently shaken when on March 10, Silicon Valley Bank (SVB) became the second largest bank to fail in United States history. Silicon Valley Bank was uniquely positioned as a financial institution, as its client base was concentrated among primarily tech companies and venture capital firms, with an unusually high percentage of deposits (approximately 94%) uninsured.

On March 8, the downhill slide began when SVB announced its intention to sell $1.75 billion of common and preferred stock to increase the strength of its balance sheet and offset bond investment losses. Earlier in the day, SVB completed the sale of substantially all of its available for sale securities portfolio, which was comprised primarily of long-term U.S. Treasuries. Although U.S. Treasury bonds are generally viewed as a relatively safe investment, the market value of bonds will decrease if market interest rates increase. If the bonds are sold prior to maturity, the bonds would be sold at a loss. The market value of bonds decreases as buyers pay less so they can achieve the higher yield afforded by rising market interest rates. As interest rates increased in 2022 and early 2023 the bonds lost value. Increasing interest rates will have a greater negative impact on long-term bonds than short-term bonds.

The company’s CEO indicated that client “cash burn” had resulted in lower than forecasted deposits, as the company’s client base of tech companies had recently struggled which in turn reduced SVB deposits. As a result, SVB sold its bond portfolio to increase its cash and liquidity. SVB sold approximately $21 billion of securities, which would result in an after-tax loss of approximately $1.8 billion in the first quarter of 2023. The proceeds from the stock sale would offset the loss from the sale of bonds. However, the company’s proposed stock offering concerned investors about the financial strength of the company. The stock price tanked 60% on March 9 and approximately $42 billion of deposits were withdrawn by the end of the day. In particular, bank customers with uninsured deposits were concerned over the availability of funds. The bank’s proposed stock offering was intended to offset the bond loss, but the stock offering raised investor concerns over the risk and liquidity of the bank. A run on the bank occurred (aided by social media), and within 48 hours insolvency resulted.

Shortly after the collapse of Silicon Valley Bank, Signature Bank became the third largest bank to fail. Spooked by the SVB debacle and contagion, customers withdrew $10 billion of deposits on March 12. The bank generally worked with crypto clients and real estate firms, and similar to SVB, had a high concentration of uninsured deposits (approximately 90%).

The U.S. banking system requires banks to hold a relatively small percentage of bank deposits in the form of cash reserves. The reason is simple. The goal is to have banks act as a conduit for economic growth. Banks keep a small percentage of deposits and make loans with the rest. Although banks do not have the cash on hand that matches the amount of deposits, the Federal Deposit Insurance Corporation (FDIC) insures up to $250,000 for each depositor. A significant demand by depositors for their money can result in the bank’s insolvency, as the bank will not have the necessary reserves.

With the SVB and Signature failures, the Treasury Department stepped in and indicated it would “fully protect all depositors.” Even depositors with balances exceeding the normal FDIC insurance level of $250,000 would be protected. While depositors were protected, investors (shareholders) would not be bailed out. The Federal Reserve also announced a new Bank Term Funding Program, which will provide greater access to cash and needed reserves for financial institutions. In essence, banks can use financial securities as collateral for Federal Reserve funding rather than selling the securities in financial markets at a loss to raise needed cash. In essence, the Treasury, FDIC, and Federal Reserve collectively worked to assure that the U.S. financial system was sound and that the SVB and Signature failures were isolated.

The causes of the SVB and Signature failures differ from the causes of the 2008 financial crisis. The 2008 financial crisis resulted from a myriad of factors, including easy credit conditions in the housing market and increasing subprime loans, the transfer of risk from lenders to investors via mortgage-backed securities, the popularity of adjustable-rate mortgages, and reduced housing values resulting from rising mortgage rates. Several major banks made risky subprime loans and investments in mortgage-backed securities tied to subprime loans. When rising mortgage rates caused the defaults on adjustable-rate mortgages to significantly increase and home prices plummeted, many subprime loans and mortgage-backed securities were virtually worthless. A massive $700 billion bailout of the banking industry (including depositors and investors) was approved by Congress in 2008. The fear was that decreased liquidity in the mortgage market, caused by the write down of mortgage securities and consequently bank assets, would dry up funds available for banks to lend. This had the potential to have a significant, detrimental impact on the economy – and other financial institutions.

As a result of the financial crisis, the Dodd-Frank Wall Street Reform and Consumer Protection Act was passed by Congress in 2010 to increase government oversight and strengthen the financial system. However in 2018, Congress passed the Economic Growth, Regulatory Relief, and Consumer Protection Act, which rolled back significant portions of the Dodd-Frank Act. In particular, the new law eased the regulations for small and regional banks (like SVB at the time) by increasing the asset threshold for the application of certain standards, stress test requirements, and mandatory risk committees.

The SVB failure will no doubt raise concerns over the regulation (or lack thereof) of smaller financial institutions. In addition, future discussions may include how to prevent company execs from selling their stock before the financial struggles of a company are publicly disclosed. The CEO of SVB sold $3.5 million of SVB stock on February 27, before the $1.8 billion loss on bonds and proposed stock offering were publicly announced. The SVB stock price was $288 on February 27 before tanking to $106 on March 9 just prior to its failure.

The Debt Ceiling: An Overview

The debt limit is the total amount of money that the United States government is authorized to borrow to meet its existing legal obligations, including Social Security and Medicare benefits, military salaries, interest and principal payments on the national debt, tax refunds, and other payments. The debt limit does not authorize new spending commitments, which are determined by the Congress and president in the federal budget process. Federal budget deficits are financed through the issuance of federal (Treasury) debt. The debt limit allows the government to finance existing legal obligations that Congresses and presidents of both parties have made in the past.

According to the U.S. Treasury, “Congress has always acted when called upon to raise the debt limit. Since 1960, Congress has acted 78 separate times to permanently raise, temporarily extend, or revise the definition of the debt limit – 49 times under Republican presidents and 29 times under Democratic presidents. Congressional leaders in both parties have recognized that this is necessary.” Not raising it would mean the U.S. would default on outstanding debt and not be able to pay existing legal obligations, which would have significant, negative, economic consequences.

The debt ceiling is set by law and historically has been periodically increased to allow the financing of government operations. According to the Congressional Budget Office, the Bipartisan Budget Act of 2019 (enacted in August 2019) suspended the limit through July 31, 2021. On August 1, 2021, the debt limit reset to the previous ceiling of $22.0 trillion, plus the cumulative borrowing that occurred during the period of suspension. The debt ceiling was raised in December of 2021 by $2.5 trillion to $31.381 trillion, which is expected to last until approximately the summer of 2023.

There is a link between federal budget deficits and the amount of federal debt outstanding. When a federal budget deficit occurs, it is financed through the issuance of federal debt (Treasury securities). Ideally, when excellent economic growth occurs resulting in low unemployment, a budget surplus occurs. This potentially allows debt to be repaid, or at the very least, not have to be increased. During periods of economic downturns with relatively high unemployment, budget deficits ensue as tax revenues fall and government spending may increase to stimulate the economic recovery. It isn’t very different from personal finance. When personal economic times are good, you want to pay down debt and save. If you don’t, you never will. When personal economic times are bad, you may have to borrow or withdraw savings for needed income.

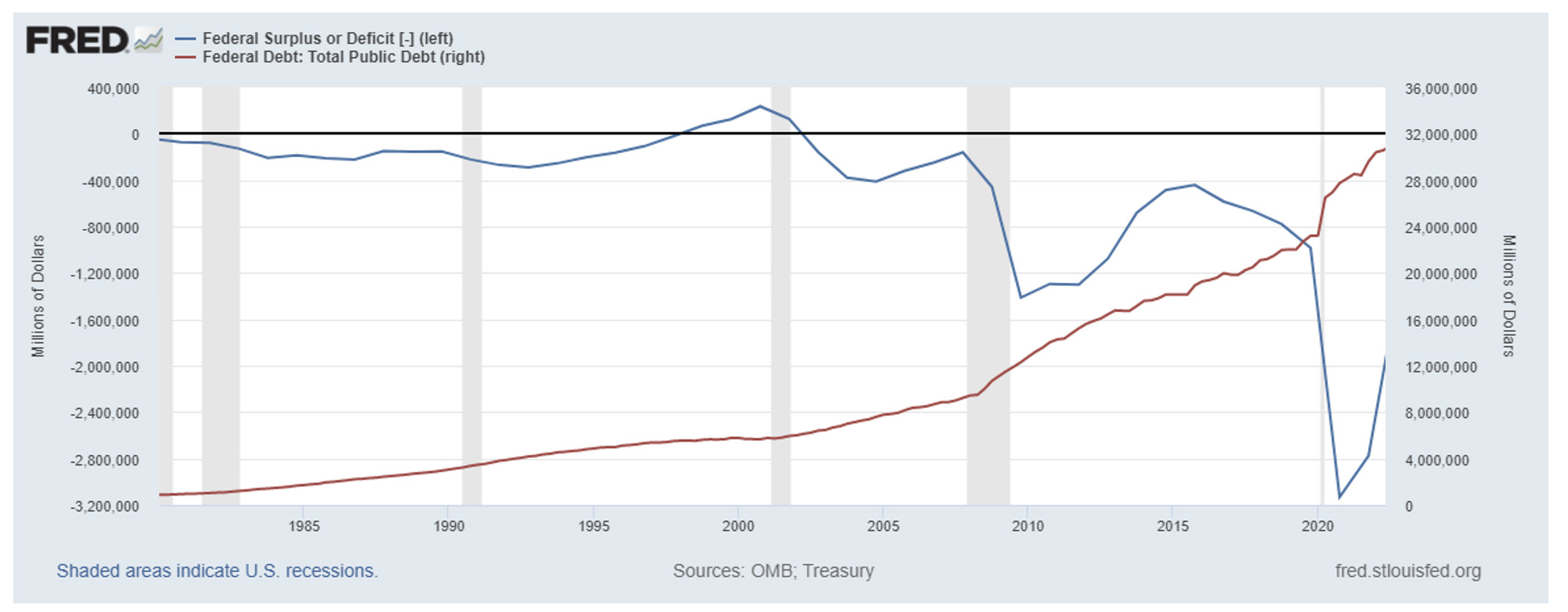

The graph below shows the relationship between federal budget deficits and the total public (federal) debt. The blue line (left axis) indicates the budget deficits or surpluses that have occurred since 1980. The onset of consistent budget deficits for the U.S. was the decade of the 1980s. Except for a brief period between 1998 and 2001 when the U.S. was enjoying excellent economic growth and the tech boom was in its internet infancy, the United States has had budget deficits since 1980. In the late 1990s, the economy boomed, unemployment was relatively low (around 4.0%), and a budget surplus resulted. An ideal mix for reducing debt. There have been three major events since the turn of the century that have significantly increased the budget deficit and total federal debt: 1) the financial crisis of 2008, 2) the tax cuts of 2018, and 3) the COVID crisis of 2020.

The red line (right axis) indicates the total public (federal) debt outstanding. Generally, the public (federal) debt outstanding reflects the accumulation of budget deficits, with subsequent budget deficits increasing the total public (federal) debt outstanding. Between 1980 and 2010, the debt rose from near $0 to approximately $10 trillion. Since 2010, the debt has approximately tripled to $30 trillion. Since 2008, two major economic downturns and the 2018 tax cut have fueled the debt increase.

Federal Budget Surplus or Deficit; Total Public Debt

Annual amount of Federal Budget Surplus or Deficit in Millions of Dollars (1980 – 2022)

The financial crisis had a dramatic effect on the deficit, with the deficit increasing approximately $1.2 trillion between the onset of the crisis in 2007 and 2009. An economic recovery began in 2010 that reduced the deficit from approximately $1.4 trillion in 2009 to $442 billion by 2015, a drop of almost 70%. The budget deficit usually decreases during periods of economic growth. That, however, changed with the tax cuts of 2018, which contributed to increasing budget deficits during a period of economic growth. Between 2015 and 2019, the budget deficit doubled to over $900 billion, despite a growing economy and the unemployment rate approaching a record low 3.5%. The Congressional Budget Office estimated in 2018 that the tax cut would increase deficits by approximately $1.8 trillion over 11 years. Contrary to the budget surplus created in the late 1990s when economic growth was good with relatively low unemployment, the new tax structure in 2018 combined with the fiscal cost structure resulted in growing deficits, despite a record period for economic growth and historically low unemployment. A budget surplus, even with economic growth and record low unemployment, no longer seemed tenable. The growing deficits were greatly exacerbated by the onset of COVID, with the deficit increasing approximately $2 trillion in 2020 to $3.2 trillion. The three major events of the current century that greatly increased the deficit, the financial crisis of 2008, the tax cuts of 2018, and the COVID crisis of 2020, contributed to the rapid expansion of federal debt.

What happens if the debt ceiling is not raised? The U.S. government may not have the needed funds to pay current financial obligations and current holders of government debt may not receive promised payments.

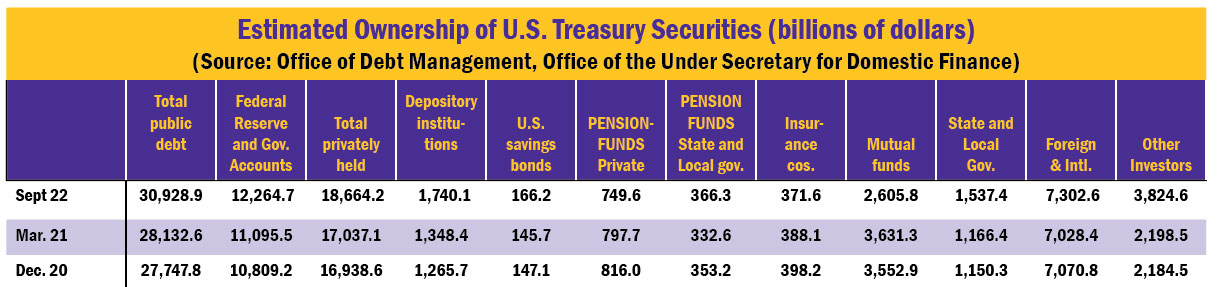

The table below shows the detail of Treasury (federal) debt ownership provided by the U.S. Treasury, and who could potentially be harmed if the government defaults. As of September 2022, a total of $30.93 trillion of U.S. public (federal) debt was outstanding. Almost $12.26 trillion was held by the Federal Reserve and U.S. government agencies, with $18.67 trillion privately held. Private investors include individuals (you could open an online account with the U.S. Treasury), large institutional investors, certain mutual funds (especially money market funds), pension funds (including private and government pension funds), depository institutions, insurance companies and other businesses, and foreign investors. State and local governments may purchase Treasury securities with excess funds. Approximately $6.9 trillion of Treasury securities were held by government agencies. Government agencies may invest in Treasury securities if they have a temporary surplus of cash. The largest government agency investing in Treasury securities – the Social Security Administration, which utilizes trust funds to pay retirement income, disability income, and Medicare.

Potential implications if the debt ceiling is not raised and default occurs:

- The government may not be able to fund needed programs or services.

- Payments to Social Security and other government program recipients may be impaired.

- The financial markets would react negatively to any default, and not be amused. Treasury securities are theoretically backed by the “full faith and credit (the power to tax and borrow) of the U.S. government”. Historically, Treasury securities have been viewed as not having default risk. However, if the U.S. fails on its promise and defaults, any future borrowing costs for the U.S. government would certainly increase. Bond market interest rates and volatility would rise due to increased risk and uncertainty.

- Defaults on Treasury bonds would cause investors losses. Investors in Treasury securities include individuals, pension plans (both private and public), mutual funds (especially money market funds), depository institutions, insurance companies and other businesses, state and local governments, foreign investors, and federal government agencies (including Social Security).

- The stock market would be negatively impacted through rising interest rates and expected economic decline.

- An economic decline would occur due to rising interest rates, decreased consumer, business, and fiscal spending, and falling stock prices. Particularly given current economic uncertainty, any default and failure to raise the debt ceiling would have a strong, negative impact on economic growth. It would be ironic, but a default would exacerbate the very problems that caused the default – budget deficits and increasing federal debt.

- Finally, a default would have major, negative impacts on the U.S. as the global economic leader and the U.S. dollar as the primary global currency. A default would likely trigger a decline in the value of the U.S. dollar as the demand for U.S. financial securities decreases. The demand for the dollar as a global currency, including its use as a reserve currency or certain countries “pegging” the value of their currency to the dollar, would subsequently decrease. This would open the door to another currency replacing the U.S. dollar in global transactions.

Summary

It has been a mixed bag for the economy thus far in 2023, with a few special add-ons thrown in. Inflation remained relatively high but decreasing, interest rates continued their climb, the labor market remained strong, and uncertainty regarding future economic growth remained. Going forward, inflation should continue to wane, the upward trek of interest rates is expected to end, and the labor market should cool as economic uncertainty remains. The special add-ons included two major bank failures and the debt ceiling saga. The two major bank failures appear to be fairly isolated as the federal government stepped in to assure depositors and prevent contagion. The U.S. defaulting on debt would be a huge mistake; the stakes are too high for the U.S. economy and its position as global, financial, and monetary leader.

For further information:

- Info from the Bureau of Labor Statistics:

- GDP Growth (and other national data) from the Bureau of Economic Analysis:

- From Eurostat:

- From the Bank of Canada:

- Global Inflation, from rateinflation.com

- From the Atlanta Federal Reserve: Wage Growth Tracker

- From the Federal Reserve:

- From the U.S. Treasury:

- From ABC News:

- Data on Treasury Debt from the U.S. Treasury:

- From the National Association of Realtors:

Kevin Bahr is a professor emeritus of finance and chief analyst of the Center for Business and Economic Insight in the Sentry School of Business and Economics at the University of Wisconsin-Stevens Point.