As 2024 comes to an end, overall, the U.S. economy is in great shape. Housing continues to be a sore spot, but the economy keeps rolling along. In 2024 economic growth was strong with more Americans working than ever as job gains continued and real wages were increasing. The U.S. stock market hit several record highs and was a global leader in providing returns to shareholders while interest rates fell.

Although consumers may still feel a hangover from recent high global inflation, U.S. inflation continued its descent from the 2022 high and was approaching the Federal Reserve’s 2% target level. The housing market remained a challenge, as relatively high financing costs and low inventory made home buying challenging.

2025 brings economic uncertainty, particularly with tariffs and trade, changes in fiscal policy with respect to taxes and government spending, and potential changes for the administration of monetary policy. Current economic momentum, however, makes the U.S. economy poised to continue and sustain its expansion. Unless an economic bump or shock occurs in 2025, moderate economic growth is expected to continue.

Economic Growth

2024

The U.S. economy continued to roll along in 2024, sustaining the expansion that began in the second half of 2020. Economic growth is measured by changes in Gross Domestic Product (GDP), which is the value of goods and services produced in a given time period. Personal consumption accounts for approximately two-thirds of GDP, and personal consumption has been the key and consistent driver of economic growth during the economic recovery, contributing positively to GDP growth since the third quarter of 2020. Between 2019 and 2023, the U.S. had stronger economic growth than any other G7 country, including Canada, Italy, Japan, France, the United Kingdom, Germany, and the Eurozone. Economic growth continued in 2024, propelling the U.S. economy to arguably the strongest in the world.

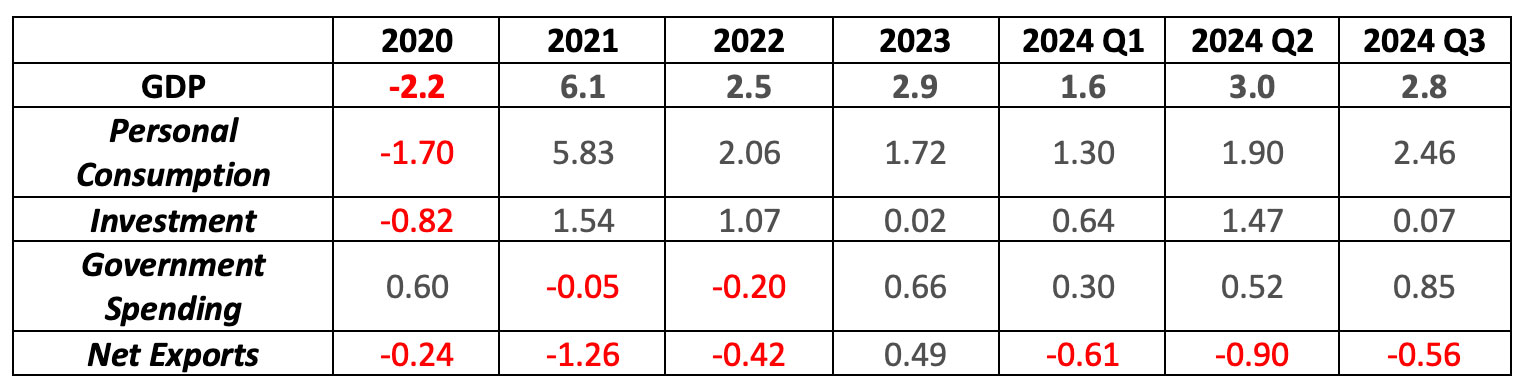

The table below shows how changes in the four components of Gross Domestic Product (GDP) contributed to the change in U.S. economic growth since 2020.

Contributions to Percent Change in Real Gross Domestic Product – Annualized Rate

Despite increasing interest rates in 2022 and 2023 economic growth remained solid, with GDP growth of 2.5% and 2.9%, respectively. After cooling to 1.6% in the first quarter of 2024, economic growth was impressive at 3.0% in the second quarter and 2.8% in the third quarter. Importantly, both personal consumption and investment spending (including business investment in equipment and inventories) made significant contributions to economic growth in 2024. Personal consumption continues to be the primary driver of economic growth, increasing GDP by 2.46% in the third quarter.

Economic Growth 2025 Preview

The United States economy typically chugs along at a pretty good pace unless there is a bump (relatively minor negative event) or shock (relatively major negative event) to derail its progress. The problem with bumps and shocks is that they are not always predictable. The key is to get the economy moving forward, precipitating a snowballing effect, where economic growth continues until something happens to stop it. When economic growth occurs, increased employment leads to more consumer spending, which leads to more economic growth. Likewise, a snowballing effect can occur in the opposite direction. If consumer spending declines, then an economic contraction continues until something happens to reverse it. If something happens to derail consumer spending, that’s where fiscal policy (spending by the U.S. government or changes in tax policy) and/or monetary policy (the Federal Reserve reducing interest rates) can be used to put consumer spending back on track.

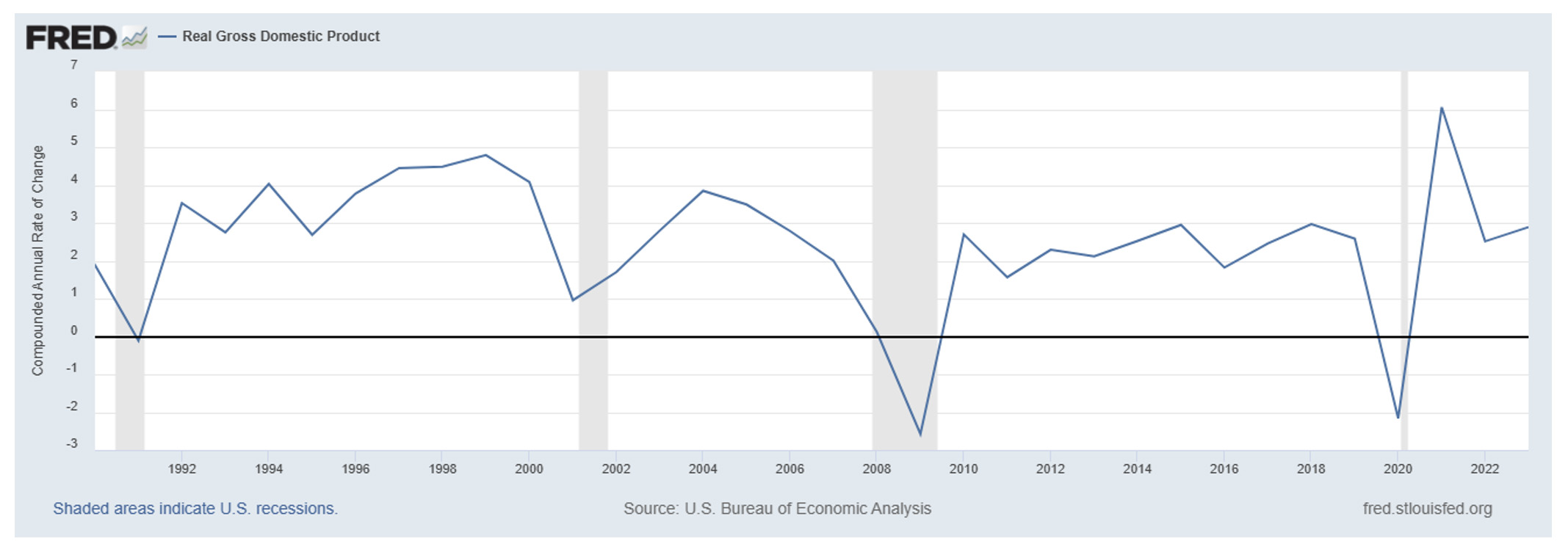

The chart below shows annual GDP growth since 1990. The shaded areas represent recessions, when GDP growth in at least two consecutive quarters was negative.

Real Gross Domestic Product – Compounded Annual Rate of Change

1990-2023

Four economic bumps or shocks have occurred since 1990 which led to recessions:

- An economic bump occurred in 1991 due to the Federal Reserve increasing interest rates and an oil price shock. By 1990 inflation exceeded 5%; the Federal Reserve countered by increasing the fed funds rate to lower consumer spending and reduce inflation. In July 1990 the fed funds rate stood at 8.0%. An oil price shock also occurred as oil prices more than doubled in 1990 in response to the Iraqi invasion of Kuwait.

- The United States began the new century with a variety of bumps to the economy. The dot.com bubble was over, with overhyped tech and internet stocks crashing back to reality. The technology heavy Nasdaq index declined over 75% between March 2000 and October 2002. The September 11, 2001 terrorist attacks contributed to the economic decline, as uncertainty and fear gripped the economy. In addition, the financial markets were plagued by accounting scandals (Enron). Although GDP growth was positive for the entire 2001 year at 1.0%, economic growth was negative for two quarters resulting in a minor recession.

- By late 2007, a major shock to the U.S. economy was beginning. Credit was easy and mortgage-backed securities allowed a transfer of risk from lenders to investors in mortgage-backed securities. Although a myriad of factors contributed to the financial crisis, rising interest rates lit the fuse for the economic implosion. As the economy rebounded from the 2001 recession and concerns over inflation grew, the Federal Reserve increased rates multiple times, from 1.00% in 2003 to 5.25% in 2006. The increasing rates not only dampened the economy, but they also paved the way for increasing monthly mortgage payments on adjustable-rate mortgages. The result was that many home buyers were not able to pay monthly mortgage payments and homes were put up for sale. Home prices plummeted, defaults occurred on mortgage loans and mortgage-backed securities, foreclosures increased significantly, and the economy and stock market began a decline in late 2007 that lasted until early 2009 (the S&P 500 declined by nearly 60%).

- In 2020 the economic shock was COVID-19. The pandemic let to record unemployment of 14.8% in April 2020 and the loss of over 20 million jobs. Economic growth returned in 2021 and continued through 2024.

Generally, economic growth precipitates more economic growth, until a bump or shock occurs resulting in a recession. Increasing interest rates have the potential for creating an economic bump, as interest rate sensitive consumer and business spending generally decline as financing costs increase. However, recent U.S. economic growth was strong enough to continue despite eleven rate increases in 2022 and 2023. In addition to increasing interest rates, other factors such as tariffs and trade wars, energy price shocks, military conflicts, and financial market declines can also cause economic downturns. The economy is in great shape as 2024 concludes; unless an economic bump or shock occurs in 2025, moderate economic growth is expected to continue. Unless repealed or modified, economic growth in 2025 should also continue to benefit from infrastructure spending (the Infrastructure Investment and Jobs Act) and investments in semiconductor manufacturing (the CHIPS and Science Act).

Interest Rates

2024

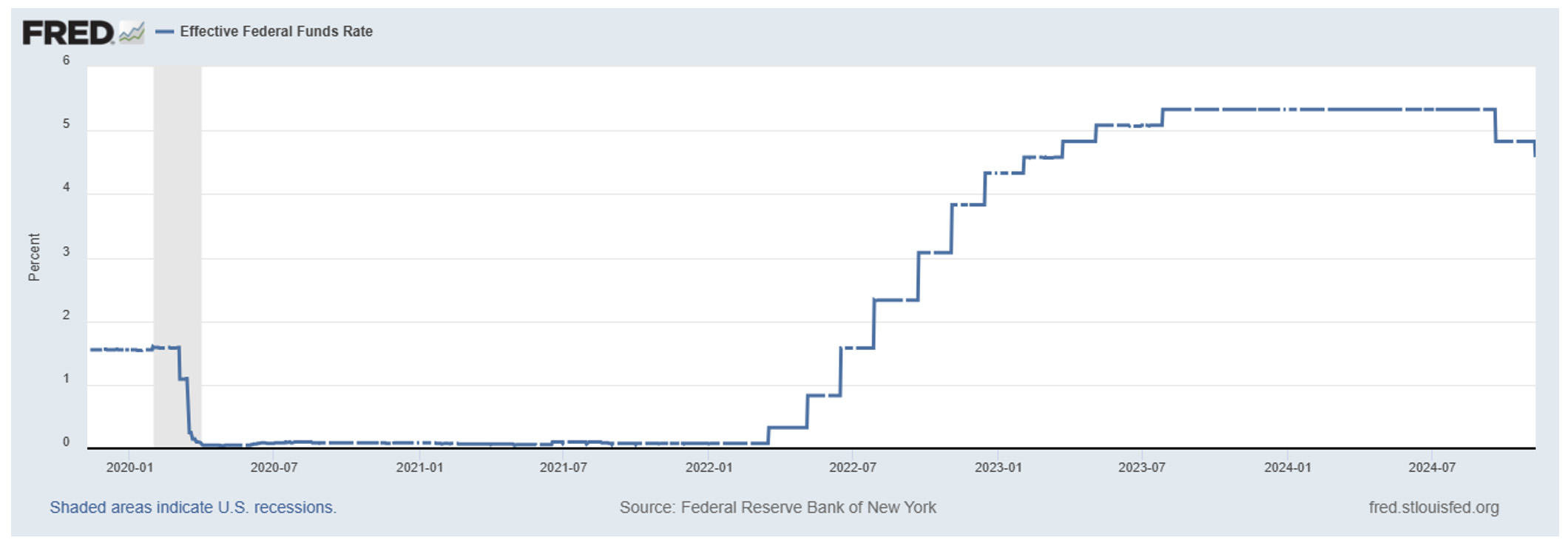

The Federal Reserve influences interest rates in the U.S. economy through targeting the “fed funds rate” – a very short-term interest rate that when changed, typically has a rippling effect through the financial markets. The fed funds rate is lowered to stimulate economic growth through increased consumer and business spending, as borrowing costs are generally reduced.

In September, the Federal Reserve finally provided a long-awaited interest rate cut, as the fed funds rate was decreased 50 basis points to a target range of 4.75%-5.00%. Another 25-basis point cut occurred in November, and the fed funds rate was reduced to 4.50%-4.75%. The rate cuts followed eleven rate increases that occurred across 2022 and 2023.The demise of global inflation led central banks around the world to cut interest rates in 2024. The rate decreases by the Federal Reserve followed interest rate cuts by the central banks of Europe, Canada, and England. In addition, the cooling of the U.S. labor market contributed to the Federal Reserve’s decision to cut interest rates. The chart below shows the federal funds rate since January 2020.

Effective Federal Funds Rate, January 2020 – November 2024

Federal Reserve policy in 2020 was driven by the expected devastating impact of COVID on the economy. Two interest rate cuts in March returned the fed funds rate to its historical low of 0.00 – 0.25%, matching the rate that was implemented during the financial crisis. The historically low funds rate, combined with fiscal policy, helped spur an economic rebound.

In 2022 the focus of the Federal Reserve, and central banks around the world, shifted to increasing interest rates to fight inflation. From a historic low of 0.00 – 0.25%, the fed funds rate hit 5.25 – 5.50% in July 2023. Central banks around the world raised interest rates to lower consumer and business spending, which in turn would lower inflation. The European Central Bank, Canadian Central Bank, Bank of England, and Australian Central Bank all implemented several interest rate increases between 2022 and 2023. Inflation was a global problem; central banks around the world raised interest rates to decrease interest rate sensitive consumer and business spending. The objective of the rate increases was to lower consumer and business spending, which in turn would lower inflation through reduced demand for goods and services even though global factors were the primary drivers of inflation.

Interest Rate 2025 Preview

The Federal Reserve has the dual mandate of achieving maximum employment with low and stable inflation through its monetary policy. The 75-basis point decrease in interest rates that occurred in September and November reflects the significant drop in inflation and cooling of the labor market. It’s a balancing act for the Federal Reserve, putting interest rates at a level that promote economic growth and maximum employment, yet also puts consumer and business spending at a level that provides low and stable inflation. Although more interest rate cuts are possible in 2025, any future interest rate cuts are subject to changing economic conditions. The labor market and the level of inflation will be key benchmarks for any Federal Reserve decision to change interest rates. A new President and administration also increase the uncertainty in 2025 for economic growth, with potential changes in tariffs and trade policies, federal government spending, labor market regulations, administration of monetary policy, and taxation.

Growing economic uncertainty was reflected by the change in short-term and long-term interest rates in late 2024. Although the Federal Reserve lowered the fed funds rate (a short-term rate) in September and November, long-term interest rates (including mortgage rates) increased. The chart below shows the change in short-term and long-term interest rates between September 26 and November 7 for selected Treasury securities and the 30-year fixed mortgage rate. Increasing long-term economic uncertainty contributed to increasing long-term interest rates, even though short-term interest rates decreased.

Yield on Selected Treasury Securities and 30 Year Fixed Rate Mortgage

The Federal Reserve will meet one more time in 2024, on December 17, setting the stage for interest rates in 2025. The CME FedWatch Tool provides insight as to what the financial markets expect for interest rates based on fed funds futures pricing. As of mid-November, the financial markets anticipated a greater than 70% chance that the fed funds rate will be cut again in December by 25 basis points.

The Labor Market

2024

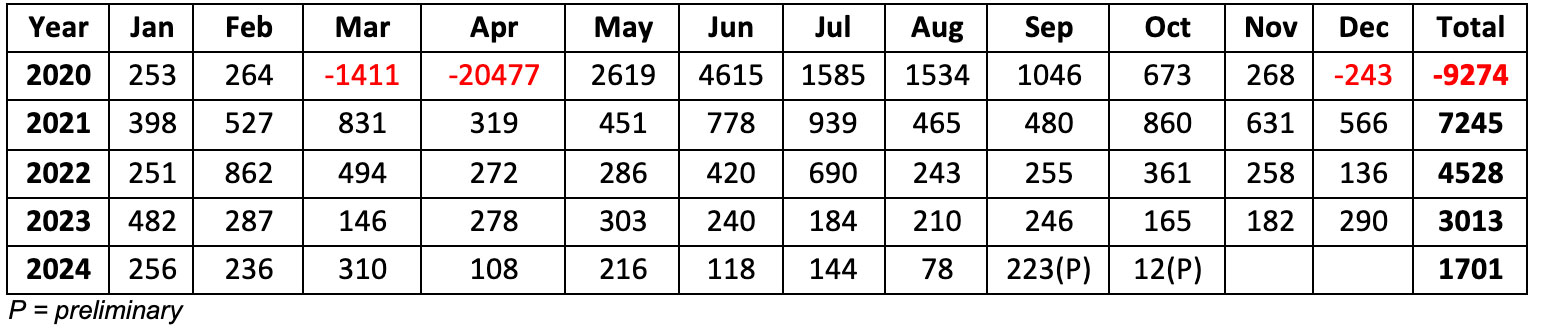

Since 2021, the U.S. labor market has been strong based on a variety of measures, including job growth, total employment, and the unemployment rate. The table below shows monthly and total annual job growth from January 2020 through October 2024. 2021 and 2022 were the top two years for job growth this century, with 7.2 and 4.5 million jobs added, respectively. The United States had job growth every month from January 2021 through October 2024. The job growth that began in January 2021 led to record employment in October 2024. The prolonged period of job growth combined with the ramp-up of interest rates by the Federal Reserve led to an inevitable cooling of the labor market, with decreasing job growth beginning in the second quarter of 2024. Average monthly job gains were 147,333 in the second quarter compared to 267,333 in the first quarter. The cooling of the labor market, combined with the significant drop in inflation, contributed to the Federal Reserve cutting interest rates in 2024.

One Month Net Change in Employment and Total Annual Change (in thousands)

January 2020–October 2024

Although the labor market has cooled, the job monthly job gains continued through the third quarter. The preliminary estimate for October job gains was only 12,000; however, employment in several states was adversely affected by severe weather, including catastrophic hurricanes. Job growth has enjoyed an impressive run. As of October, job gains were recorded in 46 consecutive months.

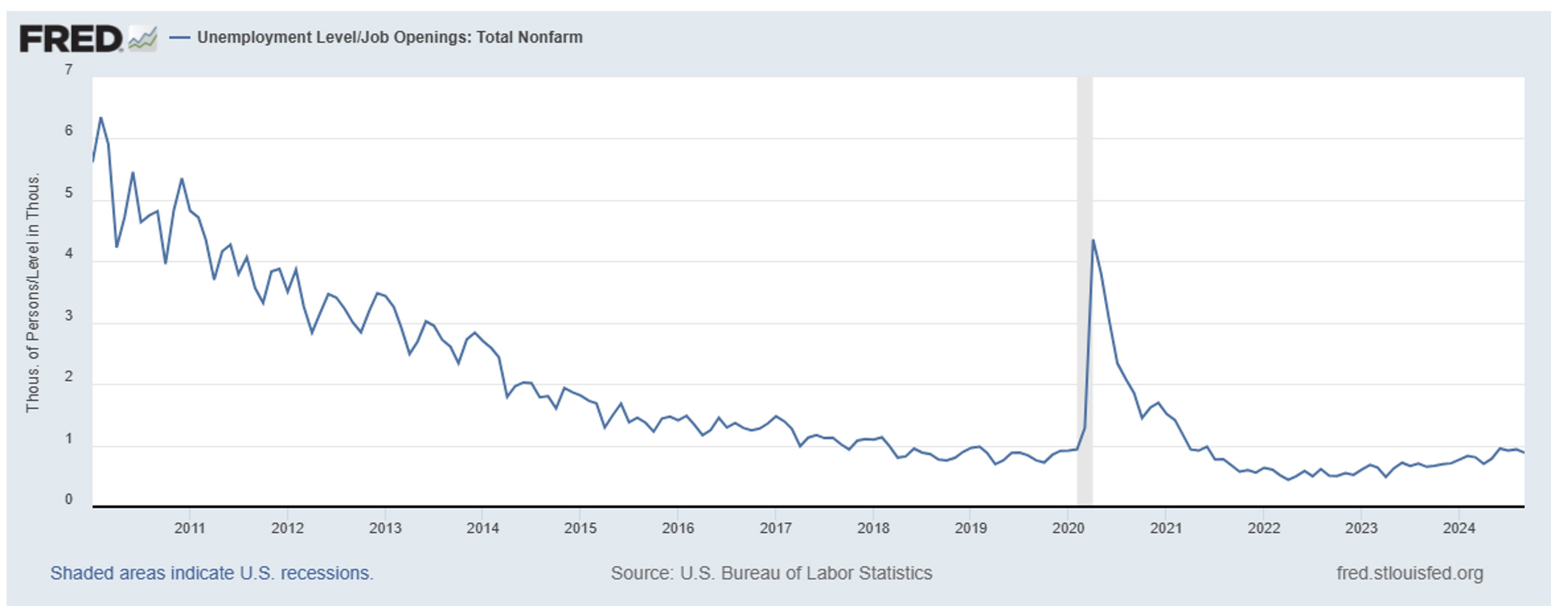

An adequate labor supply is crucial to economic growth. Balance in the labor market, between the demand for labor and labor supply, is crucial for real wages to increase at a rate that does not contribute to inflation. In 2024 that balance returned, and is demonstrated by the chart below which shows the number of unemployed persons per job opening since January 2010. In August 2024 the rate approached 1.0, meaning that there was one job opening for every unemployed person. The rate had doubled since a low of 0.5 in the second quarter of 2022 when there were two job openings for every unemployed person. The cooling of the labor market in 2024 and consequently lower real wage growth was critical to the Federal Reserve’s decision to cut interest rates. Since February 2023 real wages have increased with wage growth exceeding inflation. However, the 3-month moving average of median hourly wage growth was 4.7% in September 2024, down from a high of 6.4% in March 2023, another sign of a cooling labor market. The decrease in real wage growth reduces inflationary pressures from the labor market.

Number of Unemployed Persons per Job Opening (January 2010–September 2024)

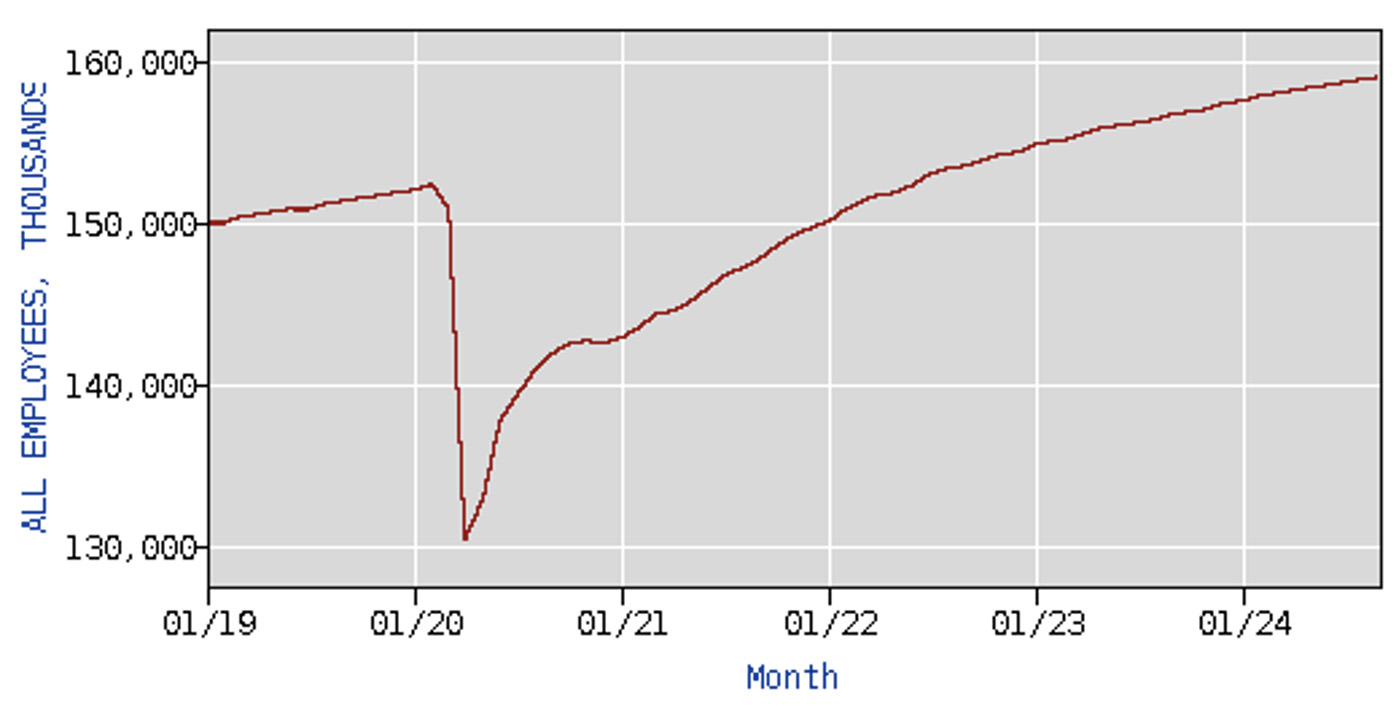

The consistent job growth that has occurred since January 2021 meant that more Americans were working in October 2024 than ever before. The chart below shows total employment (in thousands) since January 2019. A record high 159 million Americans were employed in October 2024, an increase of over 28 million workers since the April 2020 COVID low of 130.4 million. Nearly 7 million more Americans were working in October 2024 than the pre-pandemic high of 152.3 million in February 2020.

Total Employees (in thousands), January 2019–October 2024

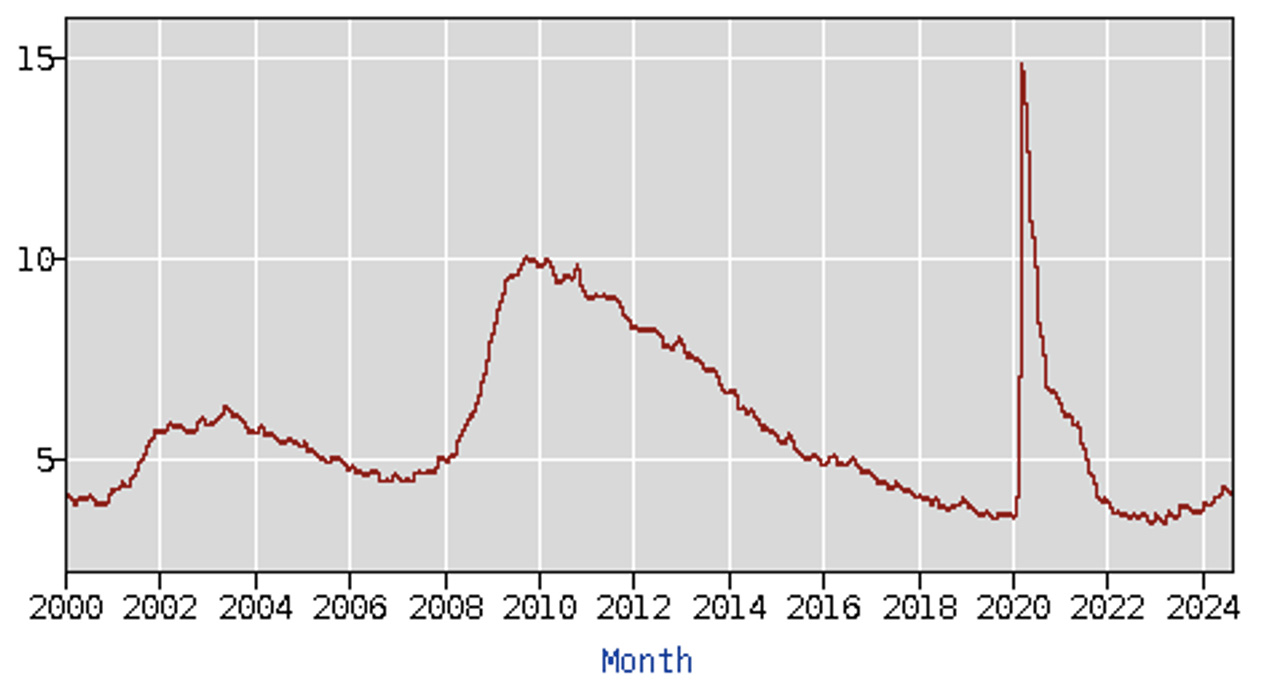

The chart below shows the unemployment rate since the turn of the century. The unemployment rate has been at historically low levels since 2022. In October 2024, the unemployment held steady at 4.1%, increasing slightly during the year from January’s 3.7%. Despite job gains occurring every month this year, the unemployment rate increased slightly. This dichotomy is due to increased labor force participation. The unemployment rate is the percentage of unemployed people in the labor force that are willing and available to work and who have actively sought work within the past four weeks. When more people enter the workforce, it is possible for the unemployment rate to increase and still have increasing total employment.

Unemployment Rate January 2000–October 2024

The unemployment rate hit a record high of 14.8% in April 2020, which surpassed the previous high of 10.8% in 1982. Despite the economic recovery beginning in May 2020, the economy stalled with 243,000 job losses in December 2020 and the unemployment rate stuck at 6.7%. The economic recovery regained momentum in 2021, and the unemployment rate gradually declined from 6.4% in January to 3.9% by yearend. The trend continued in 2022 with unemployment dropping to 3.6% in December before bottoming out at 3.4% in January 2023, the lowest rate since 1969. The unemployment rate began increasing slightly in late 2023, reflecting a cooling of the labor market and increased labor force participation. The unemployment rate of 4.1% in October 2024 was still relatively low compared to historical levels and total employment was at an all-time high.

Labor Market 2025 Preview

The labor market generally mirrors economic growth. If economic growth is strong, then so is the labor market. If economic growth is weak, then so is the labor market. The strength of the labor market in 2025 will hinge on continued economic growth. 2024 ends with the economy on a roll and moderate economic growth expected to continue, which should result in a relatively strong labor market in 2025. However, once again uncertainties result from a new President and administration, including the effects of new fiscal and monetary policies and any changes to the labor market. The labor market could also be impacted by tariffs imposed by foreign countries on U.S. exports in retribution for new U.S. tariffs.

Global and U.S. Inflation

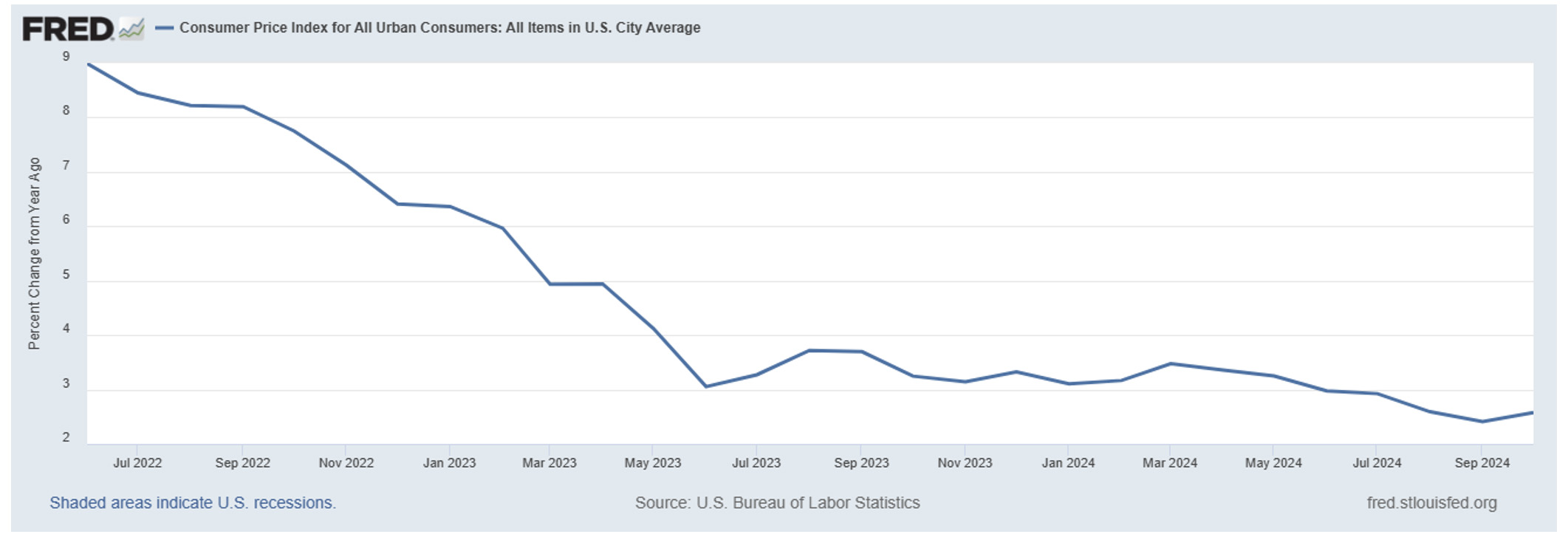

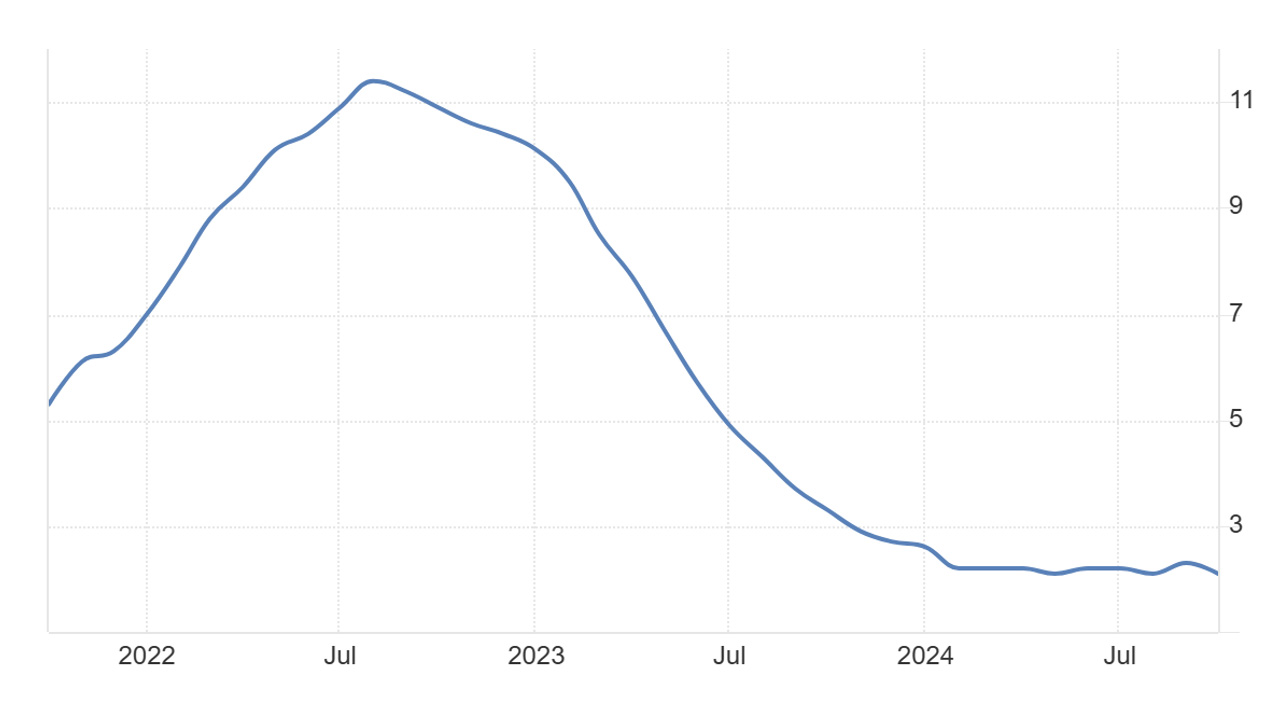

Global inflation, including inflation in the United States, has declined significantly since peaking in 2022. The decline played a major role in the Federal Reserve’s decision to cut interest rates in 2024. The graph below shows the annualized U.S. inflation rate since June 2022, as measured by the twelve-month change in the Consumer Price Index. The annualized inflation rate for October was 2.6%, up slightly from September’s 2.4%. Shelter (housing and rent) continues to be a primary driver of prices, accounting for over half of the price increase in October. Generally, inflation has consistently declined from its peak of 9.0% in June 2022 to 2.6% in October 2024. The monthly increase in prices was 0.2% in 2024 for each month July through October.

Percent Change in Consumer Price Index from One Year Ago

June 2022–October 2024

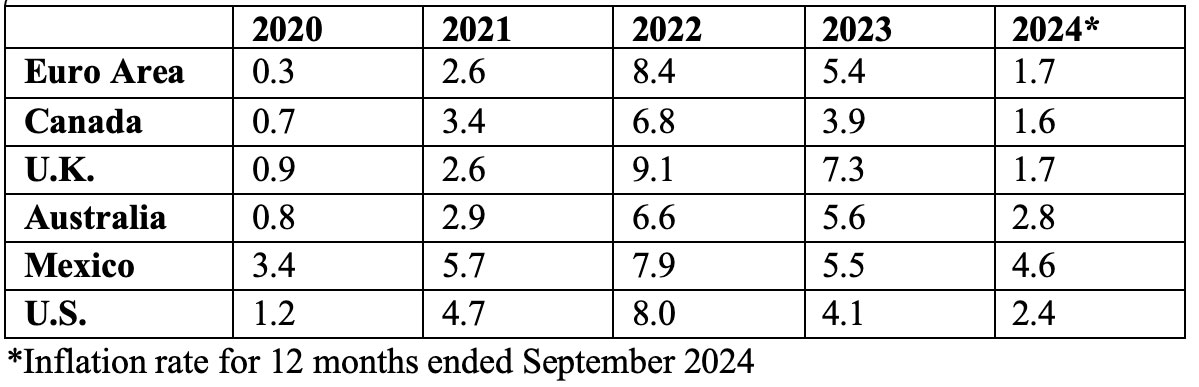

The table below shows the annual inflation rate for Europe, the United Kingdom, Canada, Australia, Mexico and the United States from 2020 through September 2024. Although there are regional differences, note that the trends in inflation are similar across most countries. The trends are similar because global factors impacted global prices. Near record or record levels of inflation were recorded for the United States, the Euro Area, Canada, and the United Kingdom in 2022. Global inflation increased in 2021 as supply chain problems appeared and global oil prices began rising due to the economic recovery. Those factors peaked in 2022, with price spikes in global energy and food prices linked to Putin’s invasion of Ukraine and lingering supply chain issues which contributed significantly to inflation. The mitigation of global factors that contributed to inflation are reflected by the significant decline in inflation that has generally occurred around the world since 2022.

Another factor that contributed to price increases for U.S. consumers was record corporate profits (and profit margins). A measure of U.S. corporate profit margins tracked by the Federal Reserve was recently at levels not seen since the early1950s, indicating that the increased prices charged by businesses exceeded their increased costs for production and labor. After-tax profits as a share of gross value added for non-financial corporations, a measure of aggregate profit margins, exceeded 15% in both 2021 and 2022, the highest level since the early 1950s. In the fourth quarter of 2023, corporate profits were approximately double what they were in the fourth quarter of 2019.

Global Inflation Rates 2020–September 2024

Food Prices

Similar to overall inflation, food prices also increased significantly around the world. The table below shows five-year food inflation over the period March 2019 through February 2024 for the United States, Canada, the Euro Area, and the United Kingdom. The food price index increase was 27.2% for the United States, compared to 25.7% for Canada, 28.8% for the Euro Area, and 30.8% for the United Kingdom. Once again although there are regional and climate differences, global factors affected the general trends in food prices similarly between countries.

Five Year Food Inflation: March 2019–February 2024

The rate of food inflation, which includes food at home and food away from home, has declined significantly in the U.S. since peaking in August 2022. The chart below shows the annualized rate of food inflation (including food at home and food away from home) from October 2021 to October 2024. In the past year, the annualized rate for food inflation declined from 3.3% in October 2023 to 2.1% in October 2024. In 2024, food inflation has generally stabilized, particularly for food at home, but food prices have not declined. For food at home, the annualized rate of inflation was 1.1% in October 2024. Food away from home has gone up over three times as much as food at home, increasing 3.8% over the past 12 months.

U.S. Food Inflation, Percent (Annualized) October 2021–October 2024

Housing and Shelter

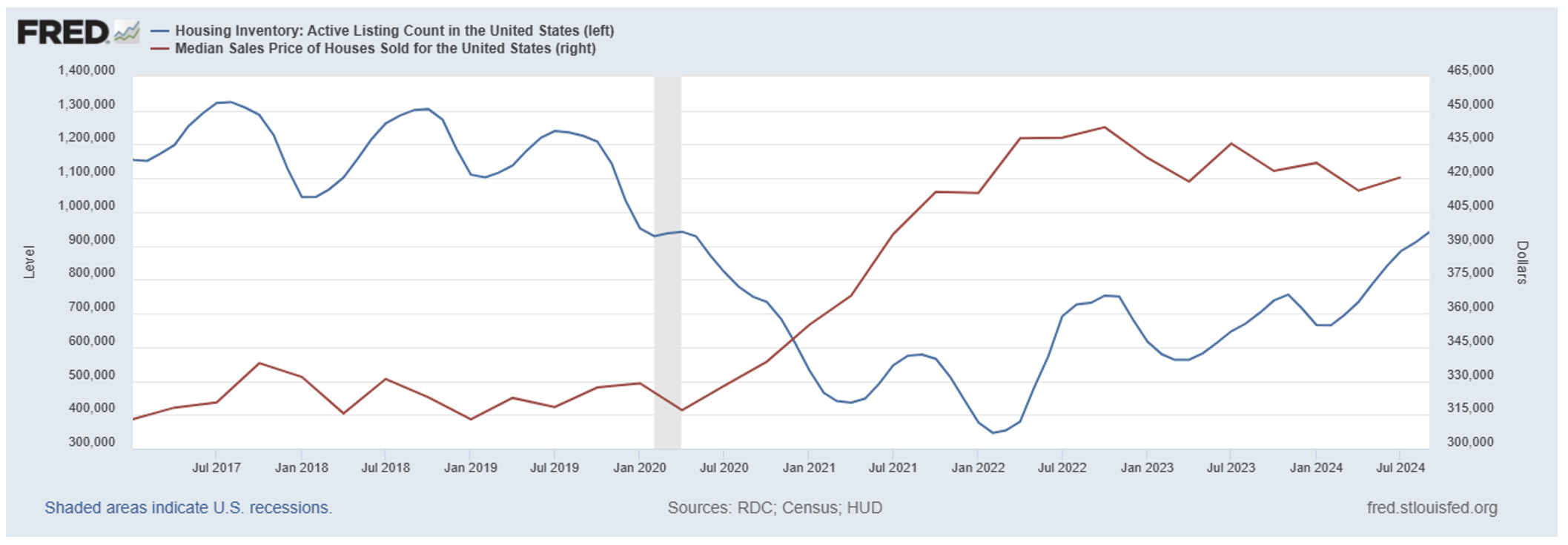

In 2024 shelter (which includes housing and rent) has been a leading contributor to inflation. Shelter comprises approximately one-third of the Consumer Price Index, and shelter prices rose 4.9% for the 12 months ended October 2024.

Housing prices began skyrocketing in the first quarter of 2020 as home listings (inventory) shrank to historically low levels. The quarterly median sales price of houses sold between the first quarter of 2020 through the fourth quarter of 2022 increased approximately 46%, nearly matching the 47% price increase that occurred over the entire last decade. The main driver causing housing prices to increase significantly was the lack of inventory, which declined significantly in 2020 and has generally remained relatively low.

The chart below shows the housing inventory (number of listings) and the median sales price for houses since January 2017. The housing inventory is indicated by the blue line (left axis); the median sales price of houses sold is indicated by the red line (right axis). The significant drop in housing inventory contributed to rising housing prices since 2020. The decline in housing inventory, combined with rising interest rates, made home buying extremely challenging.

Housing Inventory, Number of Active Listings (blue line, left axis)

Median Sales Prices of Houses Sold (red line, right axis)

Energy Production

Energy prices have been aided by the ramp up in U.S. and global oil production. According to the U.S. Energy Information Administration, the United States produced more crude oil than any nation at any time in 2023. Crude oil production in the U.S. averaged 12.9 million barrels per day in 2023, breaking the previous U.S. and global record of 12.3 million set in 2019. U.S. and global oil production decreased in 2020 due to an approximate 75% decline in oil prices which was caused by a significant drop in demand resulting from the global economic contraction. U.S. oil production declined by approximately 15% in 2020. U.S. and global oil production gradually increased beginning in 2021 as oil prices rose due to increasing demand as global economies recovered. In December 2023, average monthly U.S. crude oil production reached a record high of more than 13.3 million barrels per day. 2024 is on pace to be another record year for U.S. oil production. For the 12 months ended in October, gas prices were down 12.2% from the prior year.

The Federal Reserve and Inflation

When making monetary policy and interest rate decisions, the Federal Reserve focuses on price changes for Personal Consumption Expenditures (PCE) rather than the Consumer Price Index (CPI). Both indexes calculate the price level by pricing a basket of goods. However, the basket of goods is slightly different and the index weighting of goods is slightly different. While the two are similar, the PCE index reflects to a greater degree how Americans are currently spending their money and more quickly adapts to changes in spending patterns. The Federal Reserve seeks to achieve inflation at a 2% rate over the long-run as measured by the annual change in the PCE price index. In September, PCE inflation decreased to 2.1%, slightly above the Federal Reserve target of 2%.

Inflation 2025 Preview

Inflation has been on a consistent, gradual descent since peaking in 2022 and is on track to hover around the Federal Reserve’s 2% target level in 2025. However, as stated earlier, 2025 is wrought with uncertainty, including changes in fiscal policy (including taxes and federal spending), tariffs and trade, and monetary policy. These changes could significantly impact consumer and business spending, government spending, the labor market, and consequently the level of inflation.

Regarding tariffs and trade, new tariffs on imports will affect inflation as U.S. businesses will pay the tariffs. The extent to which new tariffs impact consumer prices will depend on the magnitude of the tariffs, how long they are implemented, and the magnitude of cost increases due to tariffs that businesses pass through to consumers. Short-term, some businesses may try to avoid the pending tariffs by building up imported inventory prior to the implementation of tariffs.

The Stock Market

2024

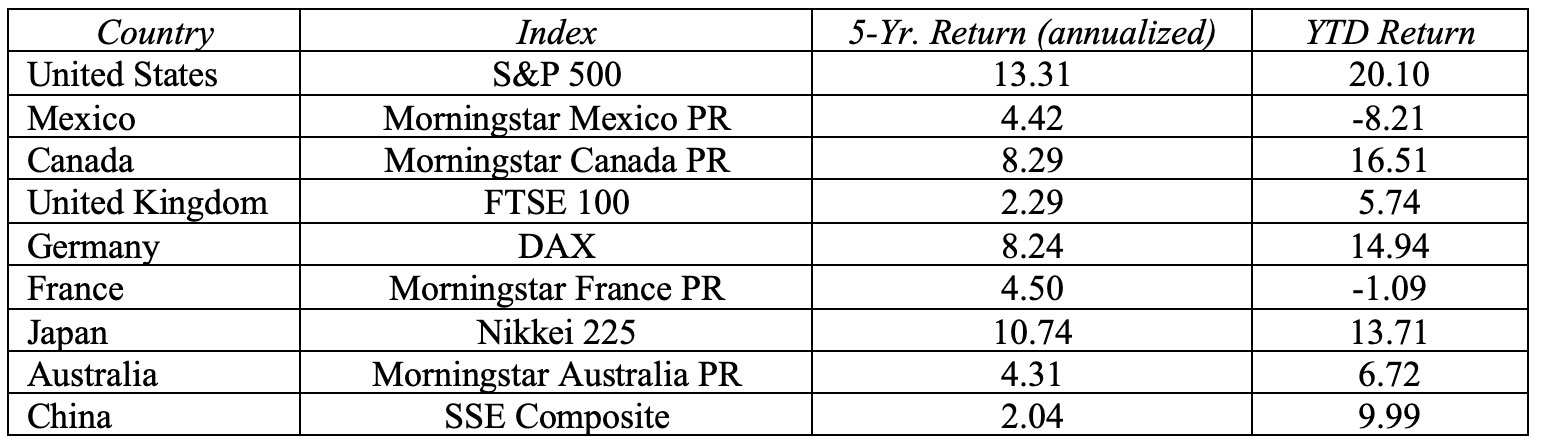

The U.S. stock market consistently hit new highs in 2024, both before and after the election. The table below compares major stock indexes for the year-to-date and five-year annualized return for the period ending November 1, 2024. The selected indexes are broad measures of stock market performance in their respective countries. The U.S. S&P 500 is a leading benchmark index for U.S. large company (large-cap) stocks, with a long-run historical annual average return of approximately 10%.

In 2024, robust economic growth led to record stock market highs, overshadowing the uncertainties created by the U.S. presidential election and wars in the Middle East and Ukraine. Through November 1, both the year-to-date and 5-year average return of the S&P 500 significantly outperformed its historical average. According to Morningstar, the year-to-date return on the S&P 500 was 20.10% while the 5-year average annual return was 13.31%. U.S. stock market returns reflect the strong U.S. economic recovery since 2020. Through November 1, relative to the stock markets in the table below, the U.S. stock market was the top performer based on both year-to-date and 5-year returns.

Global Stock Market Performance of Selected Indexes

Year-to-Date and Five-Year Returns (annualized) as of November 1, 2024

Stock Market 2025 Preview

Stock prices reflect expectations of future corporate profitability and cash flow. The expectation of lower corporate taxes and less regulation led to a bump in stock prices following the election. If economic growth continues to roll along in 2025, then the U.S. stock market will likely continue its upward climb. However, uncertainty remains as to the ultimate effect that new trade, fiscal, and monetary policies will have on economic growth and consequently the stock market.

Summary – 2024 Economic Performance and 2025 Preview

Overall, the U.S. economy ends 2024 in great shape. Economic growth has been solid since 2021, and in 2024 moderate growth continued. In the labor market, more Americans were working than ever before as monthly job gains continued, real wages increased, the unemployment rate remained at a relatively low level, and balance between demand and supply returned to the labor market. Inflation continued its decline and approached the Federal Reserve’s 2% target level. Interest rates were decreasing. The U.S. stock market hit record highs and was a global leader in providing returns to shareholders. Gas prices significantly declined and U.S. oil production was on pace for another record year. Although the housing market remained challenging due to low inventory and relatively high financing costs, overall, the U.S. economy performed extremely well. Current economic momentum makes the U.S. economy poised to continue and sustain its expansion.

However, 2025 brings much economic uncertainty. A new Presidential administration has promised significant changes, with the impact of those changes yet-to-be determined.

- Tariffs and trade will be significantly changed.

President-elect Trump has indicated that he will install a minimum 10-20% tariff on all imports, with at least a 60% tariff on Chinese goods. Tariffs are paid by the company importing the goods, not the foreign country. Any new tariffs will likely result in retribution by foreign countries, with new tariffs on U.S. exports. In 2023, U.S. imports totaled $3.8 trillion while exports were $3.1 trillion. In 2023 the U.S. population was approximately 335 million, which translates to import product demand of over $11,000 per U.S. resident. The dollar volume of imports understates the role of imports in the U.S. economy, as many imports are components for U.S. made products.

According to the U.S. Census Bureau, the top three countries for U.S. imports through October 2024 and the percentage of U.S. imports: 1. Mexico (15.7%), 2. China (13.3%), 3. Canada (12.8%). According to the U.S. Census Bureau, U.S. imports ranked by end-user product categories in 2024: 1. Capital Goods (including electrical devices, computers, and industrial machinery), 2. Consumer Goods (including pharmaceuticals, cell phones, furniture, apparel), 3. Industrial Supplies, 4. Automotive vehicles and parts, 5. Food, Feed, and Beverages.

The expected tariff policy will be significantly different from tariff policies implemented in 2019, as the expectation is that all imports would face tariffs. U.S. tariff rates peaked in 2019. The weighted mean applied tariff is the average of effectively applied rates weighted by the product import shares corresponding to each partner country. According to the World Bank, the U.S. mean applied tariff rate increased from 1.59% in 2018 to 13.78% in 2019 before declining to 1.52% in 2020. The mean applied tariff rate would be significantly higher than 2019 if expected policies are implemented.

Other changes:

- Government spending on programs and federal government organizational structure will likely change and potentially be significantly altered.

- The implementation of monetary policy and role of the Federal Reserve may be significantly modified.

- Corporate taxes may be lowered. The individual tax cuts implemented in 2018 that are set to expire in 2025 will likely be extended.

- Deportations may affect the supply of labor.

All of the above could have a significant, yet-to-be determined impact on the economy. At the very least, 2025 will be an interesting year.

For further information:

- Info from the Bureau of Labor Statistics:

- From the Federal Reserve:

- GDP Growth (and other national data) from the Bureau of Economic Analysis: GDP Growth

- From Eurostat: Euro Area Inflation

- From the Bank of Canada: Canadian Inflation

- Global Inflation, from rateinflation.com

- From Trading Economics: Food Inflation

- From the Atlanta Federal Reserve: Wage Growth Tracker

- Global Central Bank info:

- CME FedWatch Tool: CME Fed Funds Futures

- From the U.S. Energy Information Administration:

- From Investopedia: S&P 500 Average Return and Historical Performance

- From Morningstar:

- From Investopedia: What are the Top U.S. Imports?

- From the U.S. Census Bureau and Bureau of Economic Analysis:

- From the U.S. Treasury: The Yield Curve

- From Freddie Mac: 30-year Fixed Mortgage Rates

- From the U.S. Census Bureau: Top Trading Partners

Kevin Bahr is a professor emeritus of finance and chief analyst of the Center for Business and Economic Insight in the Sentry School of Business and Economics at the University of Wisconsin-Stevens Point.